When you set up your budget, how much of your paycheck should you save? Read this guide and learn how much to save and some tips to save more.

The Ascent reports that 56% of Americans have less than $5,000 in savings right now. Is that truly enough?

You know you need to be saving a portion of your paycheck, and in this guide I will share exactly how much you should save. Then, I’ll even share some tips about where to find money to save and where to put your money as you save it up.

Keep reading and you’ll discover how to get even closer to financial freedom.

How Much Of Your Paycheck Should You Save?

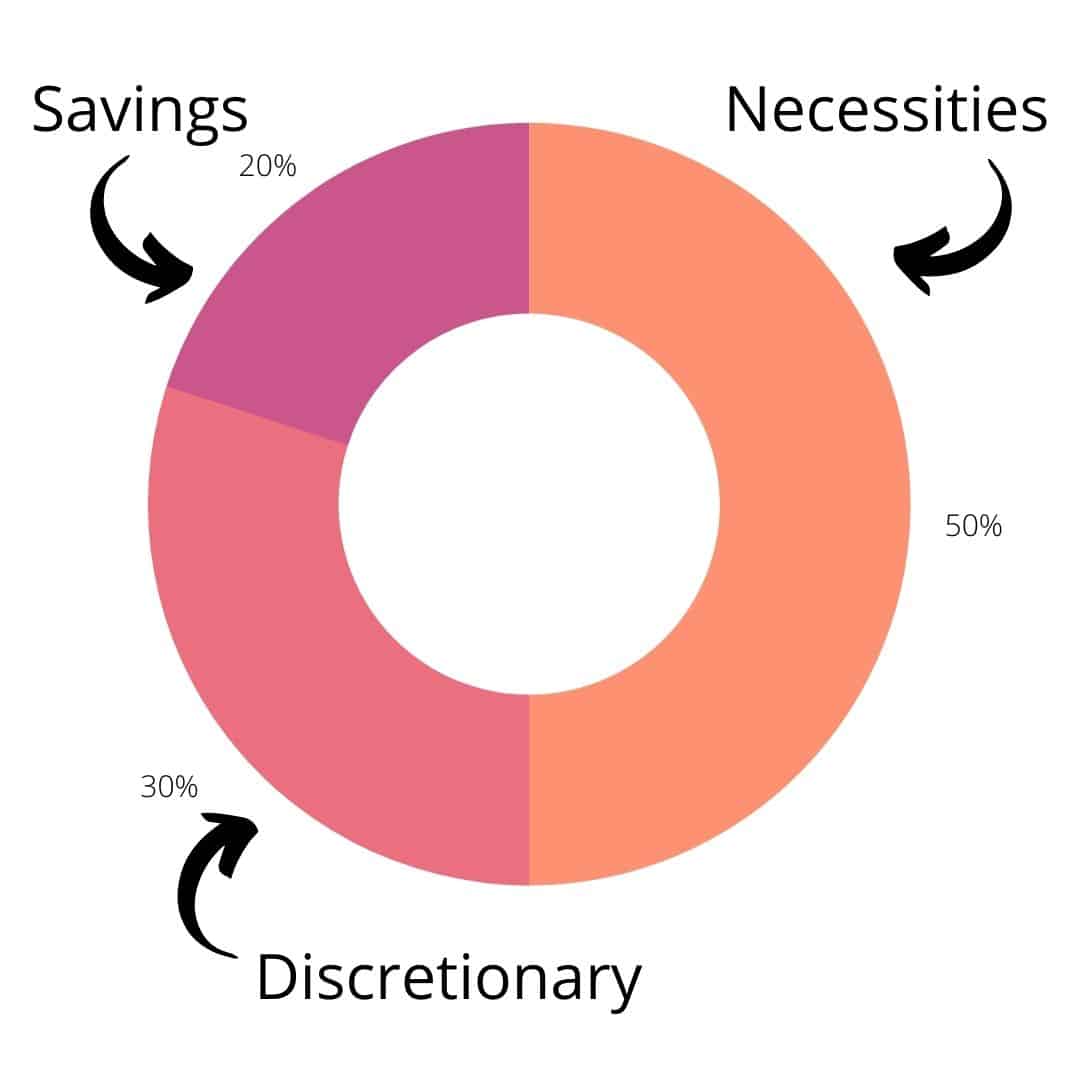

Money experts and coaches agree with Senator Elizabeth Warren when she first created the 50/30/20 rule in her book All Your Worth: The Ultimate Lifetime Money Plan.

The 50/30/20 Rule

According to Senator Warren’s rule, people should spend 50% on necessities, 30% on discretionary/fun things, and 20% should go to savings. This amount will change based on your current financial experience – how much your expenses are and what your savings goals are.

This is a general rule that is easy to remember and it will pay off when you get to retirement age.

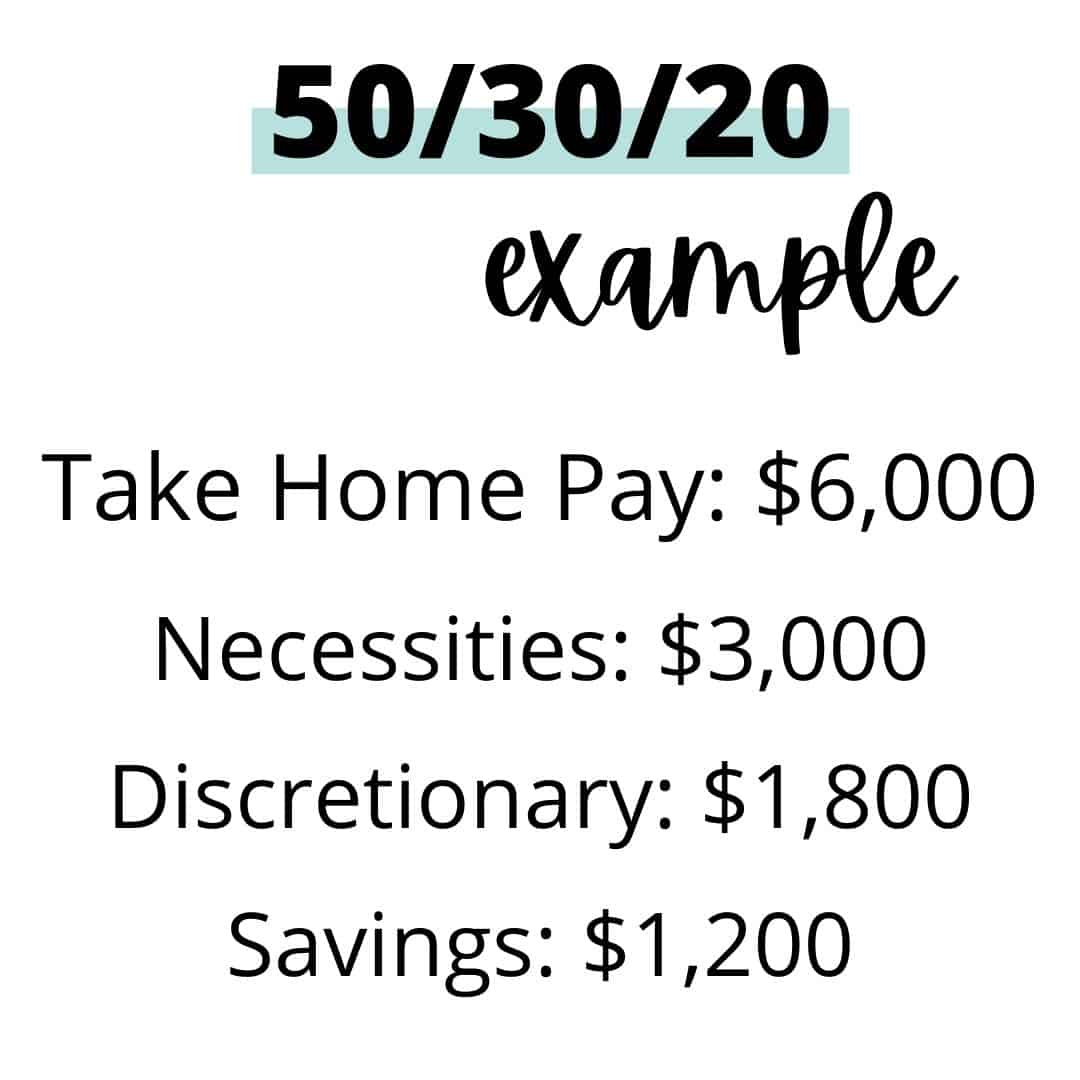

You figure this amount based on the income you bring in after taxes.

For example, if your monthly income after taxes is $6,000, then $3,000 should go to expenses like mortgage, groceries, and the like. Then, $1,800 can be spent however you want, and you put away $1,200 into savings.

Why Save 20%

Does 20% seem like too much to put into savings? It’s a pretty smart number that will protect you financially.

There are two things you are saving up for when you put that much into savings.

First, you are going to focus on building up an emergency fund. Then, you will focus on setting yourself up for financial independence.

Let’s look at what that will look like.

How Much To Keep In Your Emergency Fund

The very first thing you need to create is an emergency fund. How much you put into it depends on your lifestyle, but most experts suggest having at least enough to cover 3-6 month’s worth of necessary expenses.

To determine how much you spend each month on necessary expenses, you’ll want to write an emergency budget. This budget will only include your necessary expenses such as rent, food, gas, and minimum debt payments. No need to include Hulu, Netflix, and other subscriptions in this budget!

Once you know how much your necessary expenses total up, multiply it by 3 and then again by 6. Your emergency fund should be somewhere in that range.

Once you reach that goal amount, leave it alone. Keep that money safe and only withdraw from it if you are off work or experience some kind of emergency that goes beyond what you can afford.

If you do have to withdraw from it, build it back up as soon as you can.

Save For Financial Independence At Retirement

After you build up your emergency fund, you should then focus on saving up for financial independence and retirement.

What is financial independence?

Financial independence is when you are able to rely on income from investments and dividends instead of relying on a paycheck from an employer.

It’s almost the same thing at retirement. In fact, the definition is the same exact thing.

The term financial independence is a little different because it has nothing to do with age. Some people can reach this level in their 40s. Then, they can choose to work at little as they want.

With financial independence, working becomes an option, not a necessity. Other people call this early retirement – which it is.

Whatever you call it, save for it so that you can stop being tied to a job when you are young enough to enjoy the freedom.

How To Save More Money

If you are looking at the 20% amount and shaking your head, wondering how in the world you can ever reach that amount, let’s look at some ways you can find more money to save.

First, please understand that even if you can’t save the full 20%, it’s still important to get as close as you can. Every little bit you save is valuable. Any savings is better than no savings account at all. Your future self will thank you for making saving a priority.

Combine 401(k) With Savings Account

A fantastic thing about 401(k)s is that they are basically automatic savings that your employer helps you achieve. If one of your benefits at your job is a company-matched 401(k), then include that in the amount you are saving.

Here’s how it looks.

If you put 5% of your paycheck into a 401(k) and your employer matches it, that is already 10% savings. Now you just need another 10% from your paycheck.

Pay Yourself First

The next way to save more money is to pay yourself first, before you spend money in other places. This is just like the idea behind the 401(k). In fact, some checking accounts will automatically deposit money from your checking account to your savings account each month.

Another way to pay yourself first – if your bank has this functionality – is to round all purchases up to the nearest dollar and put the change into your savings.

Paying yourself first makes your savings account the high priority that it ought to be. Think of it this way: you’re simply taking care of your future self!

Pay Off Credit Card Debt

Another way to find more money is to lower your expenses. Focus on paying off your debt. If you have to lower the 20% savings amount in order to pay off your debt faster, do it.

It’s ok if part of your 20% savings goes towards debt payoff as long as you are trying to eliminate this debt. Then, once it is paid off, you can funnel that money directly into savings.

The best way to pay off your debt is by doing the debt snowball.

Here’s how the debt snowball works. You start off paying off the smallest debt first. Then, after that debt is completely paid, you take the monthly amount from that debt and apply it to your next debt.

Keep this pattern up until the largest debt is paid off! It’s pretty simple once you get the hang of it.

Lower Your Bills

Next, do whatever you can to find extra money by lowering your costs from your bills.

First, talk to your insurance agent. Discuss whether there is a way that you can save money on your car and house insurance. It might even be worth it to get a few quotes from other agencies.

Next, look at ways you can save on heating and electric bills. Can you insulate your home? Will investing in solar panels reduce your electric bill enough to make the cost worth it?

Finally, look at ways you can save on your grocery bill. If you need some ideas, these 22 grocery store tips are a perfect place to start.

Every time you find a way to lower your bills, keep track of how much you save and put that amount into your savings account.

Create A Budget

The best way to find more money to save is to create a budget. Go through and sort out where your money is currently going. How much are you spending on “fun money” and how much do you spend on all your other expenses?

After you see how much you are spending, you can find places to cut back and create a budget that you can stick to. This guide will help you start a new budget if you haven’t made one before.

The cash envelope method is really easy to use. Lots of people use it to help them stop spending money without thinking about it. The cash envelope method provides clear boundaries so that you have more control over your spending.

Take Up A Side Hustle

If your money is still stretched too tight to find any place you can cut back, it might be a good idea to take up a side hustle.

A side hustle is different from a job. It’s a way to earn extra money that’s on your own time. This includes things like delivering food for DoorDash or working as a virtual assistant.

If becoming a virtual assistant sounds like something you’re interested in, check out this free checklist and starter kit. You’ll be able to see if it’s something you’re interested in pursuing. As a VA you can expect to earn anywhere from $15 – $50+ an hour depending on what specialties you can offer and your experience.

With a smart side hustle, you can earn enough money to build up your savings, pay off your debt, and become financially free.

Where To Keep Your Savings

Once you have a plan for how you are going to save your money, where is the best place to keep it? That all depends on your goals and how much you have in your account.

Interest-Bearing Savings Account

If you are just starting out, the easiest place is right at your current bank in an interest-bearing savings account. It’s best to set up two-different savings accounts, however, if you are going to connect one to your checking account.

If you connect one to your checking account, you will be more likely to withdraw from it. In order to save up for financial independence, you should have a savings account that you leave completely alone.

CDs

A CD is a certificate of deposit. This earns more interest than a savings account. It has a fixed-term length and a date of withdrawal.

This is a better option if you want your money to earn more than a typical savings account and you don’t want to have access to take money out of it.

Money Market Accounts

Another option available at your bank is a money market account.

A money market account sometimes pays more interest than a savings account but you can write checks from it like you would a checking account. You are limited to 6 transactions per month.

Check with your bank and ask if a money market account is right for you. It might pay more than a savings account.

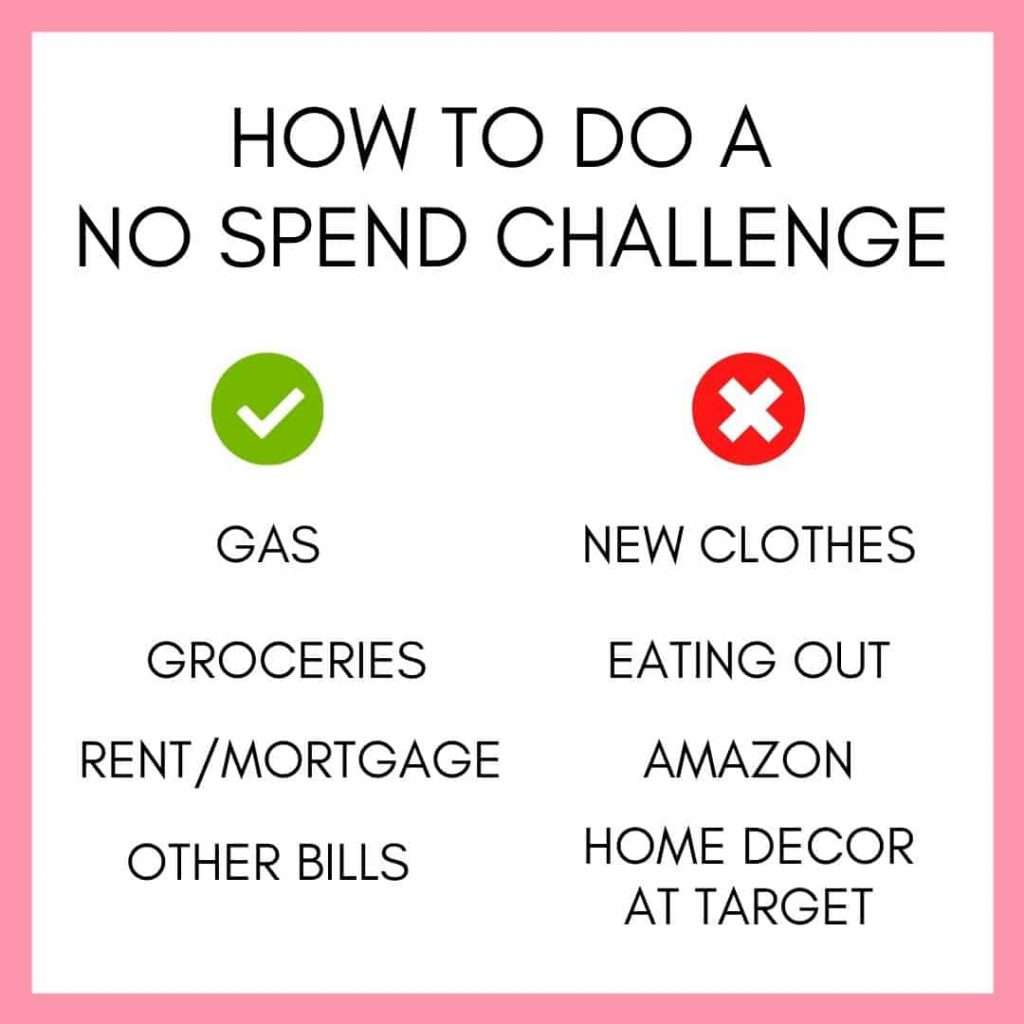

Try A No Spend Challenge

A No Spend Challenge can help you save money fast. Basically, you choose a period of time to stop spending any money. Think of it as a spending fast. The entire goal is to be more mindful of no longer swiping your debit card.

There are many ways to complete a No Spend Challenge. Whether you choose to cut out spending for a few days, a full week, or even a month, you’re bound to save money.

Final Thoughts: How Much Of Your Paycheck Should You Save?

If you’re wondering how much of your paycheck you should save, make saving 20% of your income your ultimate goal. If you do this, you will be on your way to achieving financial independence and have peace of mind that you are able to handle whatever comes your way.

If your budget doesn’t allow you to save the entire 20%, save as much as you can and keep that number as the goal. Save as much as you can and you will be financially safe and stable.