This post is sponsored by Capitalize. All opinions are 100% my own.

In this day and age, people move jobs or change careers often. In fact, changing careers is an amazing way to up-level your salary, find a job that you love, and build wealth. While a new job brings many opportunities, it’s important to tie up all the loose ends at your old job – especially your 401(k).

It’s estimated that there are currently 24.3 million forgotten 401(k)s floating out in the workspace. This means that the proper owners have moved on and left their old 401(k) behind. I don’t know about you, but when I make a move, I want to take everything with me – especially my retirement account!

But how do you actually roll over a 401(k) into an account that you have complete control over? And what if you forget to do it? Does this money just disappear? Don’t worry, I’m answering all your questions. Whether you changed jobs this year, or ten years ago – I’ve got you covered.

What happens to your old 401k when you quit or get a new job?

If you’re no longer working for your old employer, you can’t continue to make any contributions to your 401(k). While it’s still technically yours, it’s tied to your employer. Think of it this way: your 401(k) is a house and your investments live inside the house. You own the investments that are living inside your 401(k) house, but the house itself belongs to your employer.

You can leave your 401(k) there and let it continue doing its thing. Another option is to roll it over to an IRA or new 401(k) so your money is fully under your control.

If you roll your old 401(k) into an IRA that you control, then your old employer will no longer be the owner of the “house.” Instead, you will be the house owner! It’s important to know that if you have less than $5,000 invested in your 401(k), your old employer can force you to take it and leave.

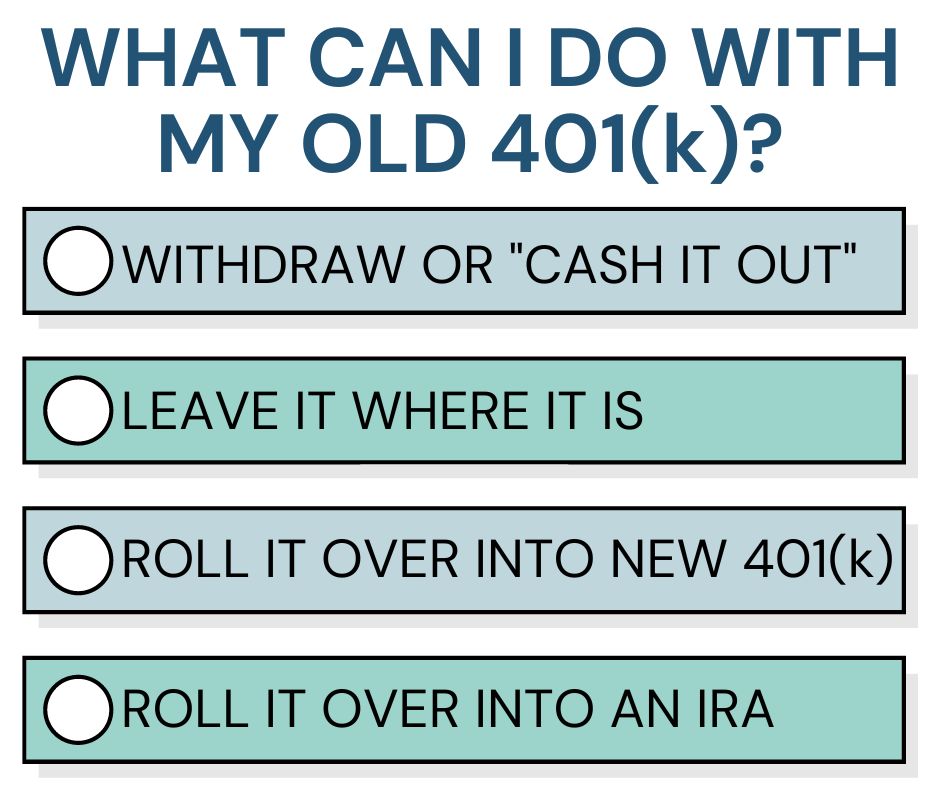

What can I do with my old 401(k)?

Don’t worry, you have options for your old 401(k) – especially if you don’t want it left with your old employer. Your options include:

- Withdraw or “cash out”: You can completely cash out or remove the money from your old 401(k) and send it straight to your pocket. While this might sound enticing, it comes with strings attached. For instance, you’ll likely pay a hefty penalty for cashing out your 401(k) before retirement age. You will also get hit with taxes. Many people believe this should be avoided at all costs and only considered in an emergency situation.

- Leave it where it is: In most cases you are more than welcome to let your 401(k) hang out at your old employer. Just don’t forget about it because you’ll want to check those fees and track its growth over time.

- Roll it into your new employer’s 401(k): Assuming your new employer offers a 401(k) plan, you can roll your old 401(k) into your new 401(k). This tax-free transfer can be a great option as long as your new employer has great investment options and low fees.

- Roll it into an IRA of your choice: If you want full control and even more options when it comes to the investments you buy, then an IRA might be the answer. You can roll-over your old 401(k) money tax-free into an IRA that you manage.

I personally had an old retirement account from my first job that I rolled into an IRA. I chose this route because I wanted full control over my investments.

Benefits of rolling over your 401(k) into an IRA

When it comes to choosing what to do with your old 401(k), I am personally a fan of rolling it into an IRA of your choosing. Here are 3 benefits that I, among others, have experienced:

Benefit #1: Save money.

I’m a big fan of saving money, especially when the savings could potentially add up to a major dollar amount. The average forgotten 401(k) account has a balance of $55,400. If your money is sitting in a high-fee 401(k) plan and is invested in poorly allocated investments, you could miss out on nearly $700,000 in retirement savings over the course of your life.

I’m guessing you want to keep every penny you can when it comes to investing – which means you’ll want full control over where and what your money is invested in. By rolling over your 401(k) into an IRA you’ll have more control over the investments you pick which can have a major impact on fees and potential return.

Benefit #2: It’s easy to manage.

The best thing about setting up and managing an IRA is that you don’t have to be an investment banker to understand how it works. Plus if you change jobs in the future, you maintain full control over your nest egg.

Benefit #3: More options.

When it comes to your 401(k) plan, you’re limited to the type of investments that you can choose from. These investments have likely been picked by your human resources department and let’s be honest – you might not like your choices. When you roll your old 401(k) into an IRA, you can choose between a seemingly endless amount of stocks, bonds, index funds, and ETFs. Basically, you have options…which everyone loves.

How to roll over your 401(k) into an IRA

Are you ready to move your old 401(k) into an IRA of your choosing?

Great! Let’s talk about how to actually make that happen!

You essentially have two options:

- Do it yourself (DIY)

- Have someone do it for you (for FREE)

Roll over your 401(k): DIY

To reclaim your 401(k) yourself, you’d have to follow the steps below:

- Identify your old employer. This can be tricky, especially if you’ve had multiple jobs or if it’s been a while since you worked at a company.

- Call and get the right documents. You’ll need to ask for documents to roll over your 401(k), fill out the paperwork, send them to the right people, and even get the documents notarized in some cases. (Truth time: this is the step where I would personally get stuck because I simply don’t want to talk on the phone!)

- Choose where to roll over your 401(k). There’s a lot of options, so choose wisely!

- Get a check and mail it to the right place. Once your paperwork is complete, you’ll receive a check with the money from your old 401(k). Make sure you send it to your new IRA provider…and make sure it doesn’t get lost in the mail.

I don’t know about you, but that’s a few too many steps for me. Not to mention it’s a little intimidating for some people. Even thinking about filling out the paperwork wrong has me sweating a little.

The DIY roll over might be a good option for some people, but I would personally rather have someone else take care of this for me…someone that’s an expert when it comes to this type of task!

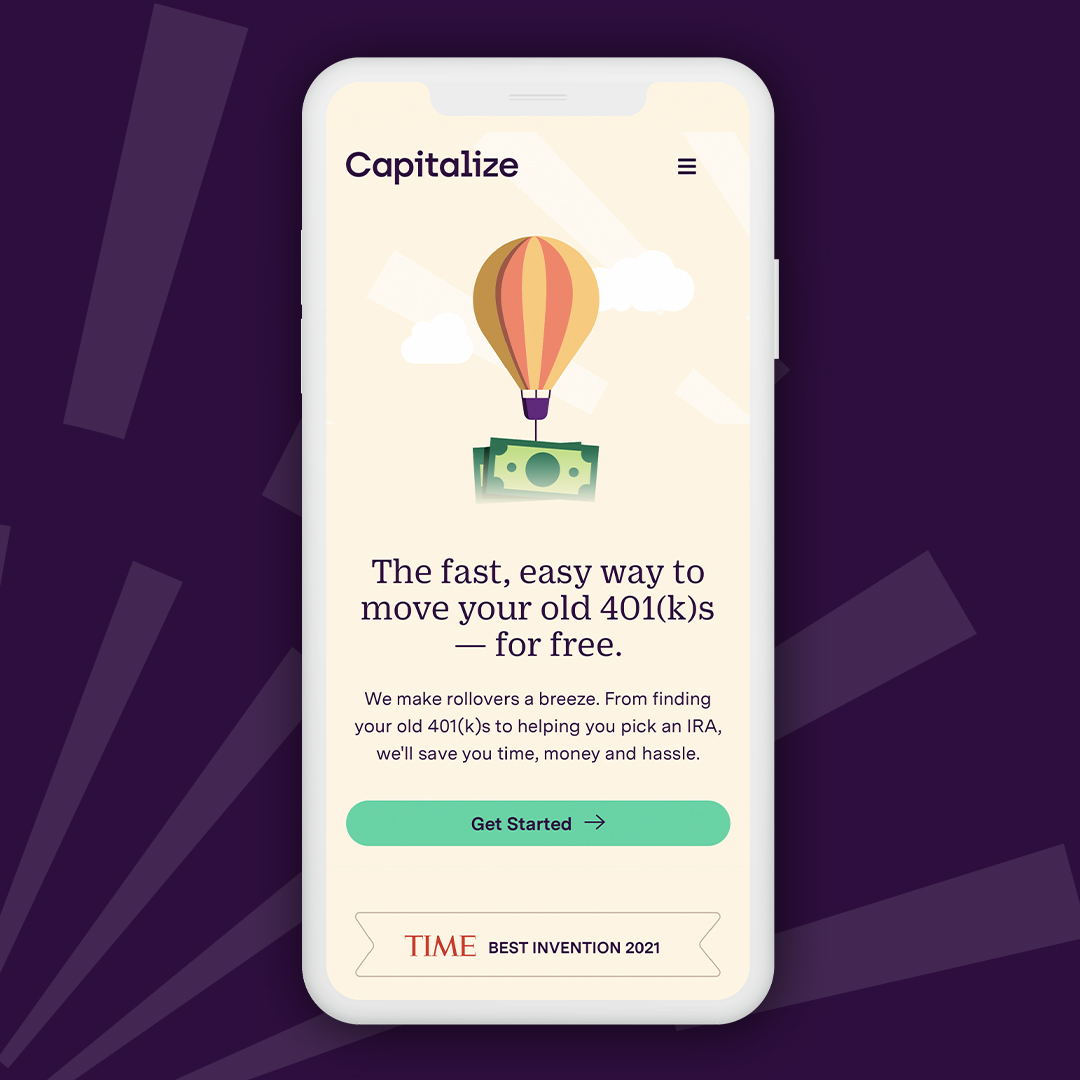

Roll over your 401(k): Capitalize

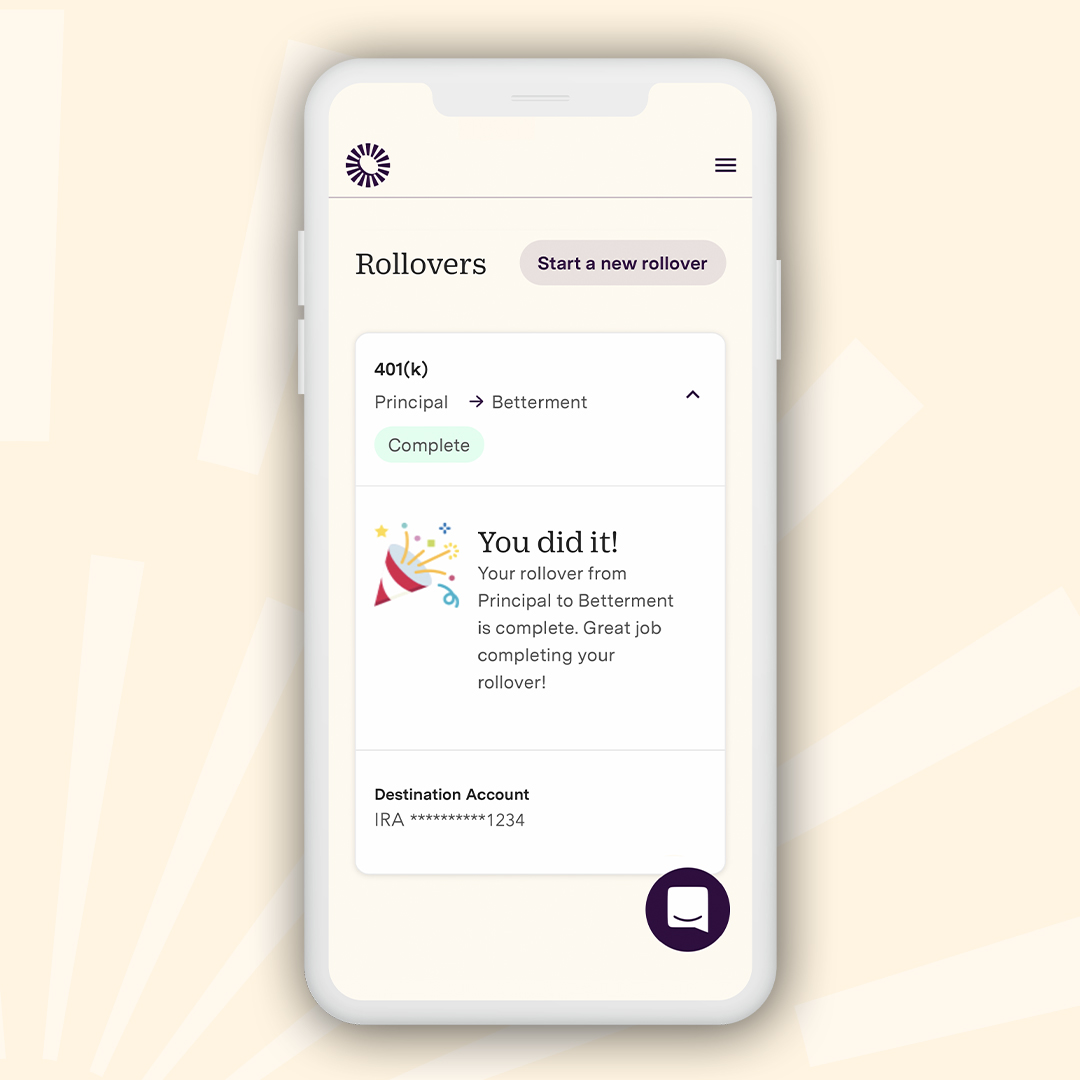

If you’re like me and want a simpler solution, then Capitalize is right for you! Capitalize is the no-stress, no-hassle way to find, combine, and roll over your retirement accounts into an IRA so you can maximize your savings.

They will manage your entire rollover from start to finish and then help you track and adjust your retirement plan. Their process is stream-lined and it means you never have to talk to your old employer on the phone (enter a collective sigh of relief). Oh, and did I mention that it’s free?!

How Capitalize works

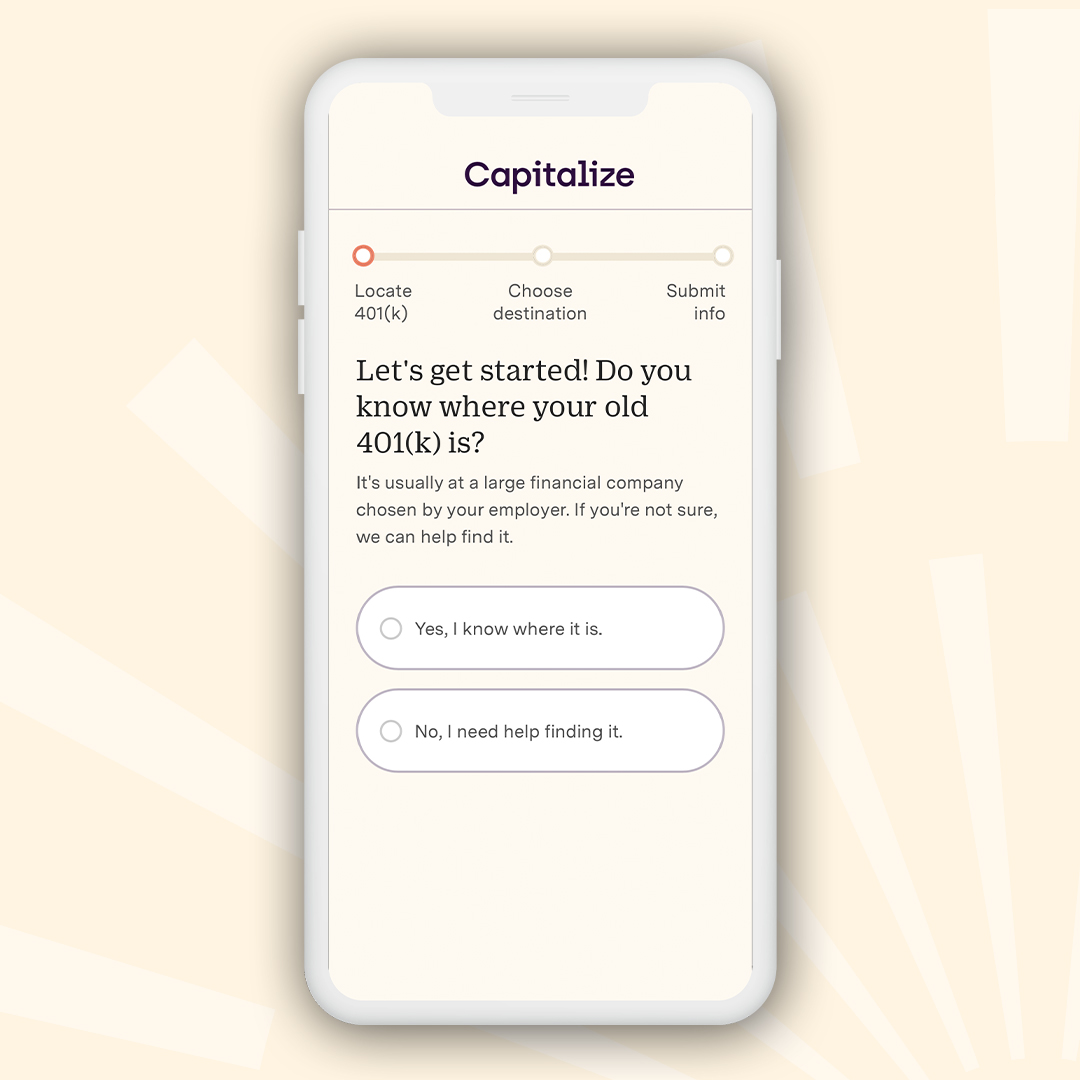

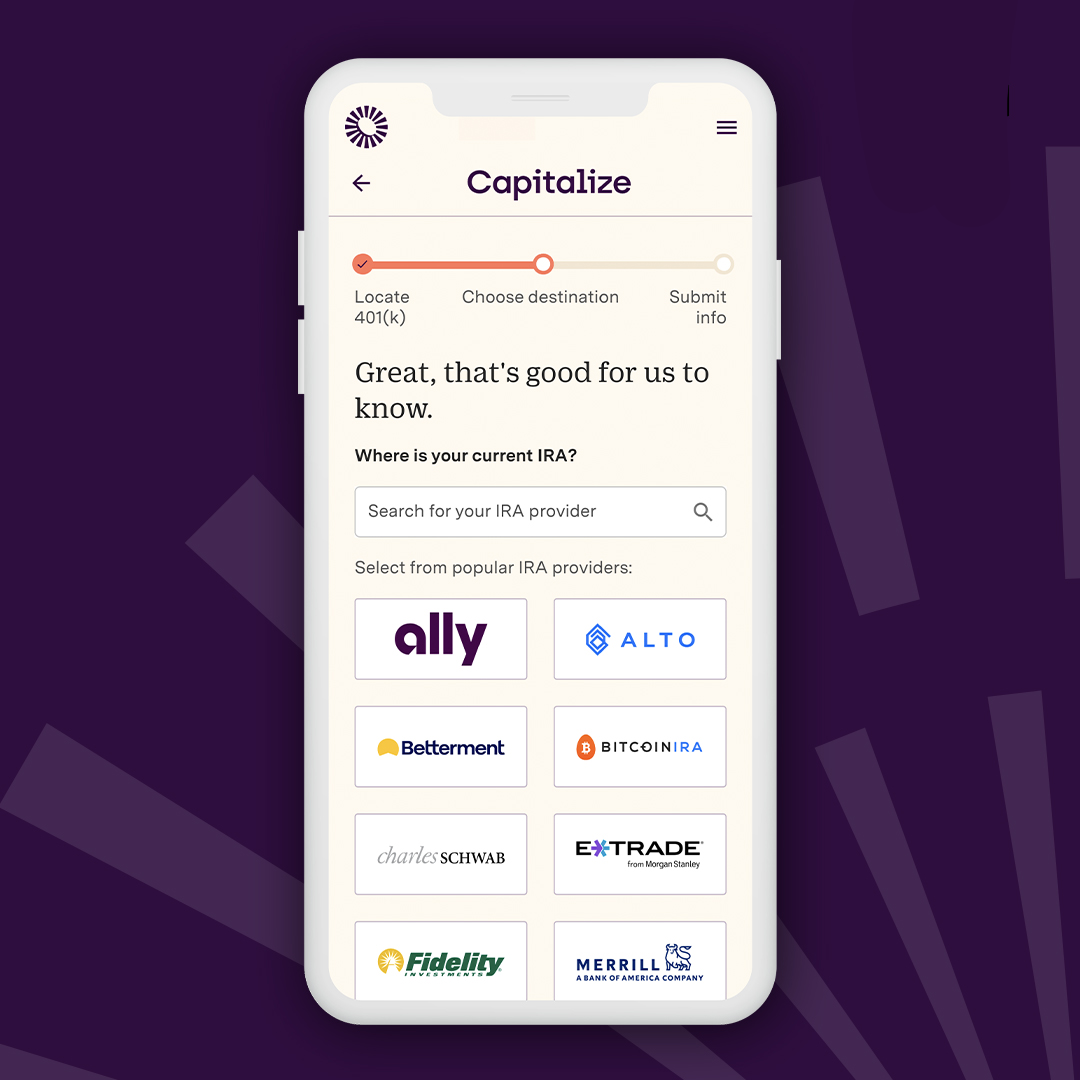

Capitalize prides itself in making the entire process of rolling over your old 401(k) into an IRA as simple as possible for you. Here’s how it works:

Step 1: Sign up for Capitalize. You’ll need to answer a few questions about your old retirement accounts and where you want to move them. They will even help you locate your old accounts or choose the best IRA for you.

Step 2: Let them do the work. Capitalize then gets to work – they will contact your old employer and 401k provider, fill out the forms for you, help you set up your new IRA, and fill you in on every step of the way.

Step 3: One final click. Once Capitalize has waved their magic wand, and your money has been moved into a new IRA, all that you need to do is make sure you choose your investments in the IRA.

Learn more about Capitalize here.

Is Capitalize legit?

If you’re asking this question, then I want to applaud you. It’s important to do your research and make sure that you’re in good hands.

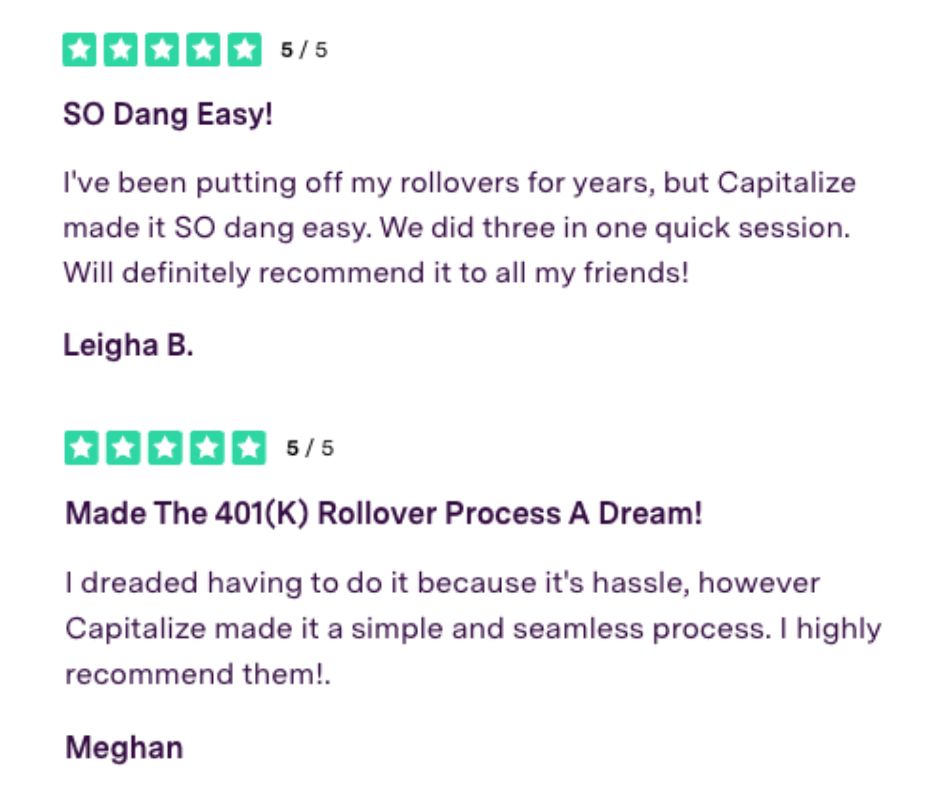

Yes, Capitalize is legit! This company was given the “Best Invention” award by TIME Magazine in 2021, has been recognized as one of the “Best Financial Apps and Services” in 2021, and has been given the “World Changing Ideas” award in 2022.

Capitalize has 4.9 out of 5 stars on Trustpilot, where you can read hundreds of reviews!

Capitalize has turned a complicated situation (rolling over your old 401(k) into an IRA) into a seamless transaction. They take an item that’s been sitting on your to-do list for years and tackle it for you!

The best part is that Capitalize is FREE for you! Yep, it’s true! They only make money if you choose to open up an IRA with one of the providers on their platforms. The provider compensates them for the referral. This means that you don’t ever pay a dime for their services.

Click here to learn more about how Capitalize can help you roll an old 401(k) into an IRA.

The Bottom Line

Your money matters, especially your retirement money. If you’ve ever changed jobs, you might have left behind an old 401(k) with your employer. If that’s the case, consider rolling it over into an IRA so you have full control over your investments. Capitalize can help make this process streamline and easy for you. Learn more and get started with Capitalize here.