Once my husband and I finished paying off debt, I knew we needed to focus on investing. Focusing on our retirement goals was our next logical step.

Side note: I wish we had started investing sooner, yes – even when we had debt. But you can’t go back in time, so I digress.

While I wanted to invest for our future, words like stock market, mutual fund, and target date index funds made my head spin.

I mean, couldn’t someone else handle this for us? It all seemed so overwhelming!

So that’s what we did. We met with a financial advisor, and handed off the task to them. It wasn’t until years later that we realized…WHOA. Their fees were freaking high.

In fact, if we continued to use our financial advisor over the course of our lives, we would end up paying thousands more over time than if we had just handled our own investments. Once I learned how these fees would impact our overall wealth, I made it my mission to learn more about investing so that my husband and I could take back control of it.

Here’s the truth: investing can seem complicated and intimidating.

We aren’t born knowing how to invest. We have to learn how to do it. We have to take time to figure out what we need to do to make our money grow – which is exactly what my husband and I did.

Naturally, we had questions along the way – and I’m guessing you do too. Which is why I’m here answering questions that real people sent me. My hope is that after reading this article you will feel more confident when it comes to investing for your future. Without further ado, let’s get to these questions.

1. Where do I start when it comes to investing? It seems so complicated.

Leslie asks “Where do I start when it comes to investing? Do I need to hire a financial advisor to invest? It seems so complicated.”

First and foremost, I think it’s smart to ask this question. Investing isn’t taught in schools and chances are likely your parents didn’t teach you about investing because they were trying to figure it out on their own. This is a learning process, and it takes time.

In fact, this reminds me of my son, James. When he was learning how to ride a bike, he was terrified of falling. Riding a bike without training wheels felt so foreign to him. He needed the extra support of training wheels as his comfort. That’s what hiring a financial advisor is like – we turn to others to help us invest because it makes us feel comfortable…even though their fees can be outrageous over time.

But once James was able to practice, learn, spend time on his new bike, and invest in himself, he was able to confidently ride a bike without training wheels. His bike was no longer foreign. The coolest part is that he now feels so free. I love seeing him zoom down the sidewalk toward the park on his bike. He has the confidence that he never had before.

Investing is like learning how to ride a bike without training wheels. You can hire a financial advisor and they can help you, but you won’t have the confidence to invest if you don’t learn how to do it yourself. You’ll feel free when you realize that you actually have everything it takes to build your own wealth. You just need to be intentional and spend time on the bike, practicing and learning. Just like James did.

That’s why I think your very first step when it comes to investing is to commit to learning about the process. Ask questions like “what is the stock market?” and “how do index funds work?” Read books about investing and listen to investing podcasts. Take a course or search for answers online. Investopedia.com is an amazing website that breaks down investing terms and is a wonderful resource if you’re wanting to learn more about investing.

By committing to learn something new about investing every day, even if it’s just reading one article online or taking one class, then you’ll be well on your way to becoming a confident investor. I know, because that’s exactly how I learned about investing!

2. How do I get over my fears that I will lose money?

Sera said “The stock market has been so volatile for my entire life! How do I get over my fears that I will lose money?”

First and foremost, it’s incredibly normal to have fears around investing. Especially since nothing is guaranteed. Yes, you can lose money. No one can accurately predict what will happen with the stock market. But there’s one thing we know for sure: when money is involved, our emotions can get in the way.

It happens so much that there’s even a name for it: emotional investing. Emotional investing is when you invest based on emotions. For many people these emotions come down to greed or fear.

Now, I fully believe that our emotions serve a wonderful purpose in our life – especially fear. In fact, fear is our brain’s way of protecting us. Fear starts in the amygdala, a part of your brain, and sends a signal to your body that it’s time to fight or flight. Once fear kicks in, you become hyperalert, your pupils dilate, and your heart rate rises.

In many cases, this is a wonderful thing. For instance, if I’m walking my dog around the lake in our neighborhood and suddenly see an alligator hanging out on the sidewalk (I do live in Houston, so this is 100% a possibility), then my fear will kick into high gear. I’ll either fight that sucker or run and get my sweet dog out of harm’s way. In case you didn’t know, dogs are a tasty snack for alligators.

However, when it comes to investing, it’s best to keep your emotions, or fear, out of the picture. When the market is volatile, which it is, then your best option is to tell your emotions to take a backseat. Instead, make decisions based on pure facts. When you zoom out and look at how the stock market has performed over the past thirty, fourty, or fifty years then you’ll see that losing all your money is not likely. You’ll also see that it’s completely normal, and expected, for there to be ups and downs in the market. In fact, it would be odd if there wasn’t!

So the next time your fear kicks in and you start thinking that you’ll lose all your money if you invest, then it’s time to tell your brain “thanks for trying to protect me, but I’ve got this” and make a decision based on facts.

Another great option if you’re prone to fear is to consider investing in index funds that track the total stock market. This is exactly what I do! Index funds allow you to own a small slice of every company in the stock market or in a particular index, such as the S&P 500. For me to lose all my money, every company in the stock market would have to go bankrupt.

3. How do I start investing with a small amount of money?

Kristi wants to know “How do I start investing with a little amount each month?”

If you don’t have a ton of money leftover each month to invest, you might be wondering if it’s even worth your time and energy to start investing. Chances are you would rather spend that money on something else. I completely understand because I have had this exact same thought!

However, I fully believe that investing now, even with just a small amount of money, can help you create a positive financial habit in your life. This means that investing will become a no-brainer for you. It will be something that you do every month without question – especially if you automate your investing.

The best part about getting started with investing, even if it’s just a small amount of money, is that it allows you to actually see the power of compound interest in action. It’s one thing to understand how compound interest works, but it’s completely different to see your money make more money. It might even motivate you to start investing more!

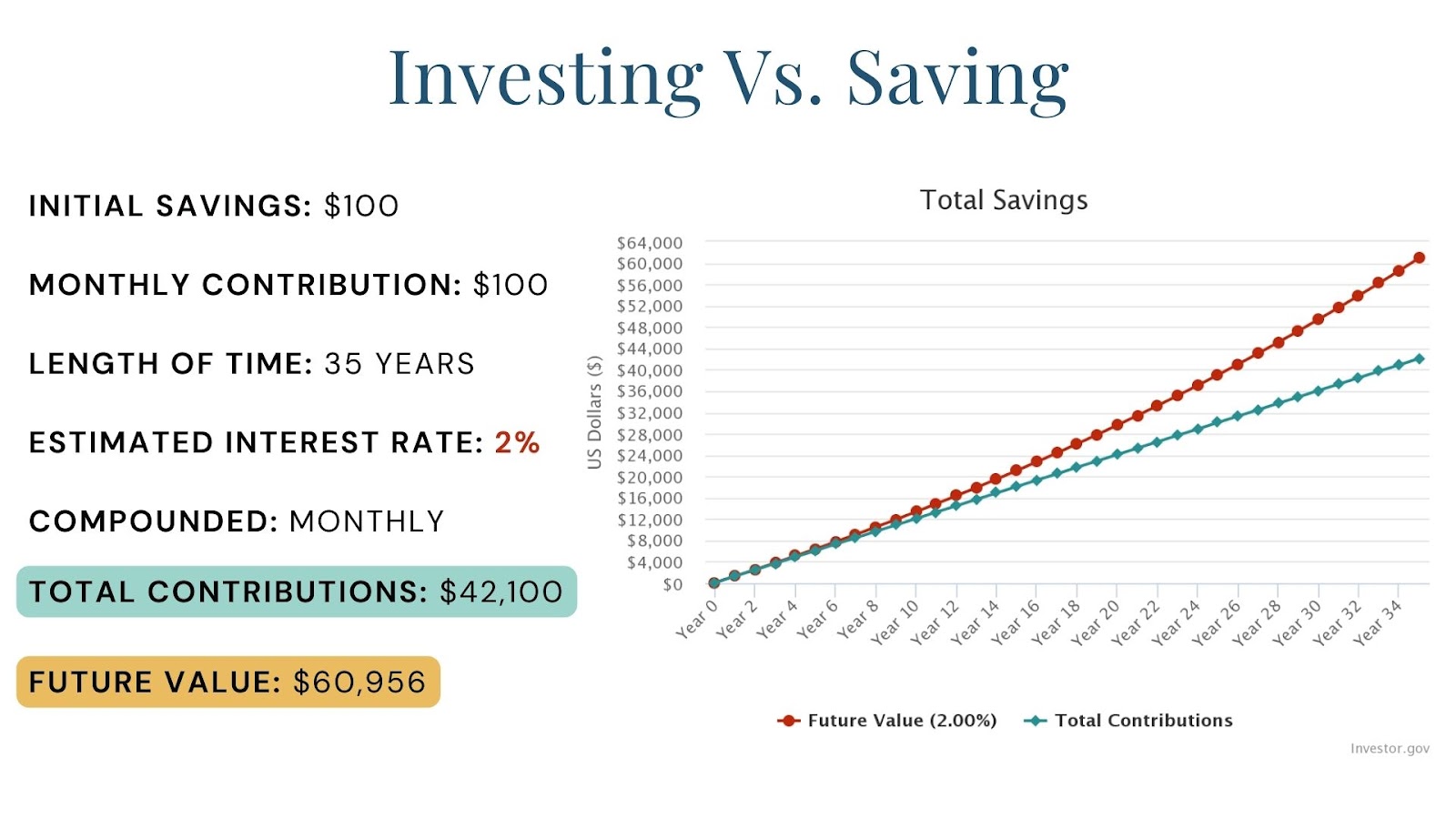

I love a good example, so here’s one that I love. Let’s say you decide to save $100 each month in a high-yield savings account that has a 2% interest rate. After 35 years you will have $60,956. However you only contributed $42,100 to this account. The rest grew over time thanks to the interest! Not too bad!

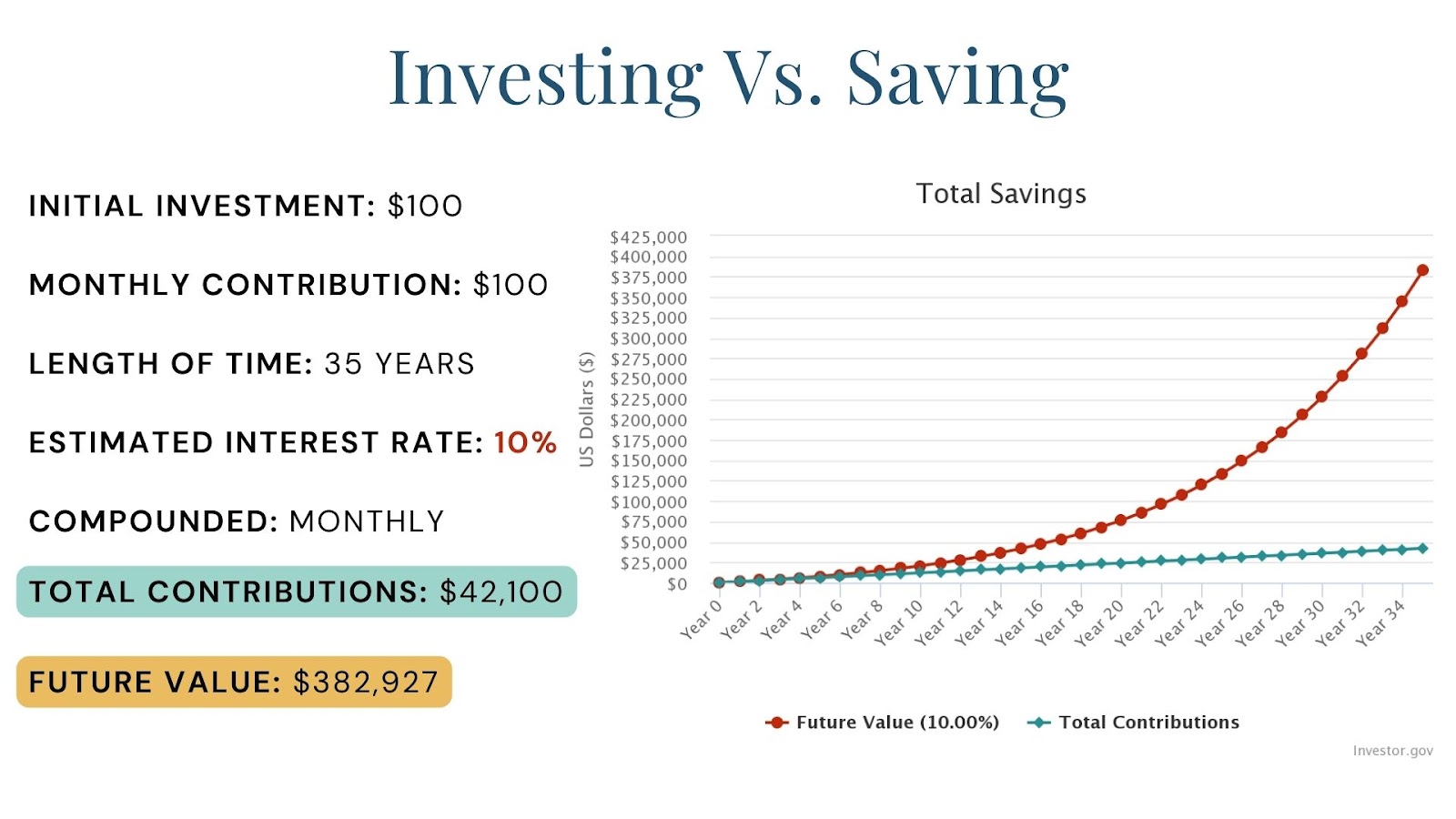

But let’s say that you decide to invest that $100 in the stock market instead. The stock market has averaged about a 10% return over the past 50 years, so let’s use 10% as the interest rate. After 35 years you would have $382,927! Meanwhile you only contributed $42,100. The rest of that money grew over time thanks to compound interest.

This example highlights that when it comes to investing, every dollar counts. You don’t need to have an extra $500 laying around every month to get started. Even $50 can make a difference when it comes to your future. Remember: the more time your money has to grow in the stock market, the more money you’ll have!

4. What happens to my 401(k) if I leave my job?

Stephanie asked “What happens to my 401(k) if I leave my job?”

This is a great question and one that is important to consider. Gone are the days where employees stay at the same company or the same job for their entire career. People are excited to make the switch between companies and careers because they want an increase in pay or more flexibility at home. Heck, I wanted both!

But when you leave behind a job, you might be leaving behind a 401(k) as well. Right now it’s estimated that there are 28 million left-behind 401(k)s. What’s even worse is that 2 out of 3 Americans don’t know what they’re paying in 401(k) fees. Meaning, you could be paying hefty fees that might make retiring sooner harder to do.

However the fear of leaving behind your 401(k) shouldn’t keep you from moving up in your career. If you don’t want your old 401(k) hanging out with your old employer, then you can roll it over into an IRA. This allows you to potentially save money over time as long as you choose a low-fee IRA. It also gives you the opportunity to manage your retirement account yourself. You can pick and choose the funds you want to invest in. AKA you won’t be limited to what your HR department offers when it comes to investing for retirement.

The entire rollover process can be overwhelming due to the paperwork and phone calls alone. That’s why I personally recommend Capitalize. They are a free online concierge platform that will help you find your old 401(k)s and roll them over into an IRA of your choice that you have full control over.

In other words, their team of experts do all the calling, paperwork on your behalf, and streamline the entire process. One of their recent reviews is from Angie who said “Capitalize made this SO easy for me. Not only did they call my 401k company and then me so I didn’t have to sit on hold, they knew questions to ask that I would have never known to ask. They sent me step by step instructions and I could not be happier.”

If dealing with your old 401(k) has been on your To-Do list forever, then it might be time to hand it off to Capitalize. Click the link in my show notes to learn more about Capitalize or go to inspiredbudget.com/capitalize to get started.

5. Can I invest even if I have debt?

Bella’s question is a common one! She asks “Can I invest even if I have student loan and car debt?”

Here’s the thing about investing while in debt: it’s truly a personal choice. Obviously, you don’t want to take away money that you could be using to pay off debt. However, investing early on gives your money an opportunity to grow over time which can lead to more wealth in the future.

Here’s the general rule of thumb that I suggest, but feel free to take it or leave it. If you have any debt with an interest rate above 10%, then focus on paying off higher-interest rate debt first. Anyone with high-interest rate debt knows how frustrating it can be to make payments but see so much of the payment going straight to interest. This keeps you from making as much progress on your debt free journey as you might like. If that’s the case for you, then pay it off as soon as you possibly can. This way, you can focus on investing and growing your money after.

If you don’t have any high-interest debt, then feel free to start investing, even if it’s just $100 each month. You can still work on paying off debt, but investing earlier can have a major impact on your overall finances.

Of course, this is a very personal choice. Our family did not invest while we were in debt and I wish that we had. Make the best decision for you.

6. How should I adjust my investments when I get a raise?

Sarah wants to know “When I get a raise, how should I review or adjust my investments?”

First off, I love that you’re thinking this way. This is a wonderful example of someone who has the right mindset around investing and money. I say this as someone who used to think the exact opposite!

In the past, if I would have received a raise, I would immediately ask myself what I can buy more of, and spoiler: I would have never spent my newfound money on investing.

I am a firm believer that we should be able to enjoy the money that we earn. Meaning, celebrate your raise. Enjoy a percentage of the money and spend it on whatever brings you joy! Likewise, it’s important to increase your investing rate as well. For instance, if you bring home $500 extra each month thanks to your raise, maybe you could set aside $200 for spending and send an extra $300 each month to investing. If that feels like too much, then pull it back to an even 50/50. Spend half on what you want and invest the other half.

It’s important to not let lifestyle creep get the best of you when you get a raise. This is essentially when you start spending more money as you make more money. Then before you know it, you aren’t saving or investing as much. While some lifestyle creep is okay (our family has experienced it personally), don’t let it get out of hand.

Investing for Retirement: The Bottom Line

As you learn more about investing for your future, more questions will come up. Remember that it’s okay to learn during this process. In fact, it’s encouraged! The more questions you ask, the more confident you’ll become when learning how to build wealth. The biggest thing you can do now is jump in and get started!