I’m not going to lie to you – I’m a little bit nervous about releasing this episode.

Partly because I’m talking about something that I have experience in, but not professional training in. And also, because I’m going to be very vulnerable and open here. I’m going to be sharing something about myself that not a lot of people know about. And usually, when they do find out about it, they’re pretty shocked. And that is: I struggle with anxiety and depression. Before I get into the nitty gritty, I need to add this disclaimer: I am not a therapist. I am not a psychiatrist. My experiences with the subject that I’m speaking on today stem from my own personal experiences.

Mental Health & Money

I was diagnosed with clinical depression at 13. I was suicidal and therapy saved my life. I spent years of my life battling with depression and anxiety and attended years and years of therapy. I used to feel like there was a weight sitting on my shoulders. The only time I didn’t feel that weight was when I was sleeping. So I thought “Hmmm what if I was asleep all the time?” BECAUSE I was depressed, I couldn’t rationalize this thought…and that’s terrifying.

Do you want to know the last thing that was on my mind during times like this? My finances.

If you’ve ever been depressed or if you’ve ever dealt with anxiety, or if you’ve ever been impacted by financial stress or worry, you understand that our money doesn’t care about our mental status. Life still goes on. Bills still need to be paid. We have to continue working to bring in money. This is why I think it is imperative for those of us who struggle with depression or anxiety to create safeguards and systems for our money so that when our mental state isn’t the best, our money can still do what it needs to do.

Tips for managing your money when depression or anxiety hits

Ultimately, I believe that our mental health is more important than our financial health. However, our mental health greatly impacts our financial health. And likewise, our financial health greatly impacts our mental health. This is why it’s so important to create money management systems WHEN we’re in a good mental state so that when we need to take care of ourselves mentally, we can take a step back while our money runs on autopilot.

Follow a plan

The first thing is I want you to follow a plan. More specifically, a SIMPLE step-by-step plan that is easily implemented and can run on autopilot or can easily be handed off to someone we trust while we focus on our own recovery. Following a plan when it comes to your money allows you to preserve the mental energy you need to prioritize your mental health. So for me, my plan looked like:

- step 1: save up an emergency fund.

- Step 2: learn how to write a budget that works for me

- Step 3: track my expenses

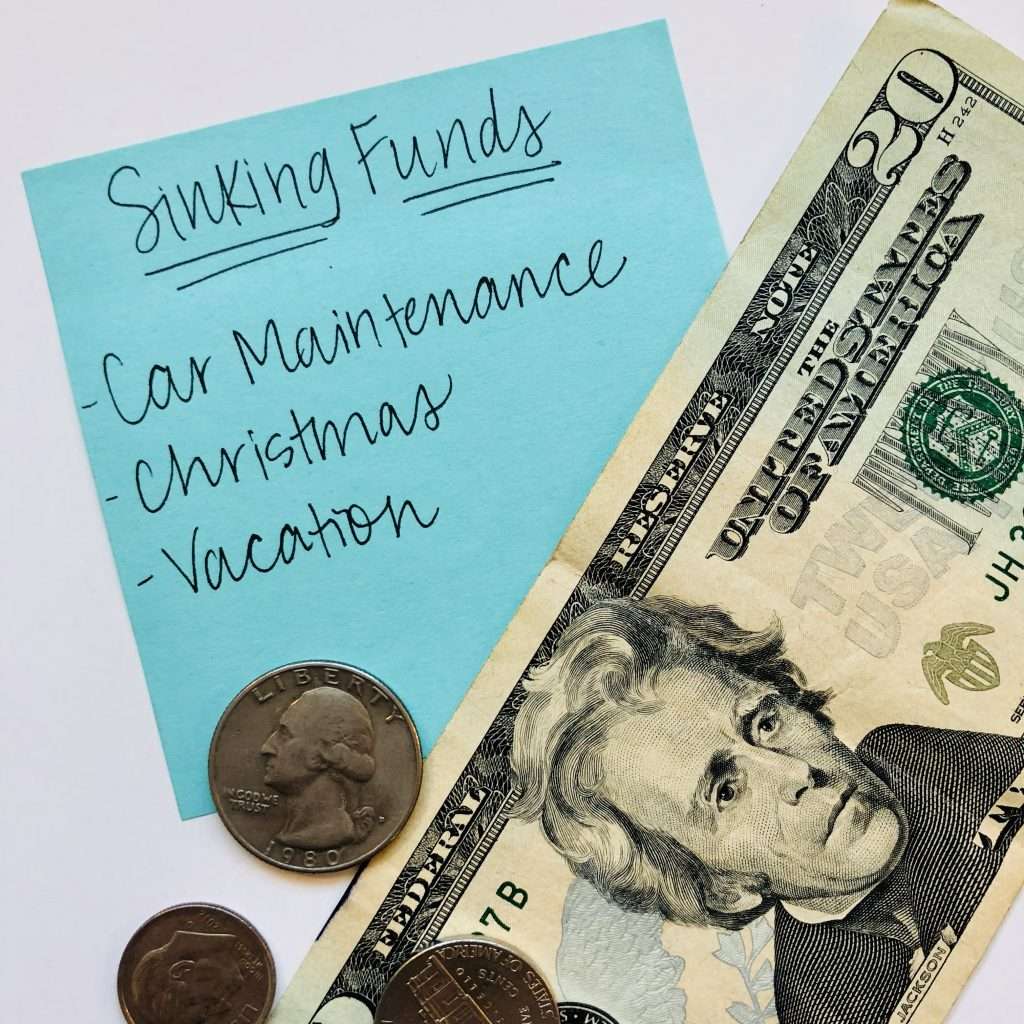

- Step 4: utilize sinking funds

Having a plan in place to manage your money that operates as a quick checklist takes the guesswork out of managing our money, making it easier to pay our bills, prepare for our future, and focus on ourselves during those times where we need to prioritize our mental health.

Build your savings & sinking funds

Sometimes when depression or anxiety hits, our expenses increase. Your savings can help cover this. Simply having more money in savings lessens our overall financial anxiety. Think of what makes you anxious: making dinner? Covering the increase in therapy costs? Paying for new medication? Create a sinking fund for it.

Whenever I have personally gone through an episode of depression or anxiety, the first expense that increases is my therapy bill. I go from paying my therapist once a month to once a week which increases my monthly bill by $300. Similarly, as I have tried different types of medication to manage my mental health, my medication bill increases anywhere from $10 to $125 per month. My restaurant bill also increases because honestly, when I’m in survival mode, I’m not going to cook dinner!

Having extra money set aside in savings can help cover increase in such costs really helps ease my anxiety as I start to prioritize my mental health. So, consider building up your savings and creating sinking funds so that when you do deal with depression or anxiety, you have money to pull from and you’re not adding the stress of putting things on a credit card or going into debt. That way you can spend more of your mental and emotional energy on recovery.

Automate everything as much as possible

When depression or anxiety hits, it’s sometimes hard to complete even the smallest of tasks. Automating your money gives you LESS to do when you or someone you love is faced with depression or anxiety.What to automate:

- Bills

- Savings

- Debt payments

Know what makes you anxious when it comes to money

Are there certain times when you’re feeling more anxious than others? Or are there certain categories of your budget that cause anxiety for you? Noticing patterns surrounding our money can help us prepare in advance so that when costs arise, we don’t panic.

For me, I found I was actually more anxious at certain times of the month – typically the week before payday. Why? This was when our account started getting really close to zero. So what I did was start including a buffer in our budget to help ease my anxiety. I also found that any unexpected expenses that had to do with our cars – for whatever reason – caused me the most anxiety. So, we set up a car maintenance sinking fund to help alleviate a lot of that stress!

Ask for help

When my I’m struggling with my mental health, I just don’t have the capacity to do everything that I normally could. Whether it’s cooking dinner, running errands, or performing my daily money routine, I find when I’m struggling mentally, these tasks fall to the way side. Depression and anxiety can be all-encompassing, and sometimes we really just need a partner or a friend to help us get through it. Open up to your partner or a friend about what you’re going through. Tell them directly how they can help you when you are struggling. Be very open and straight forward. We have to be willing to ask for help so that we can focus on getting better.

Another way to ask for help is to seek out therapy. Find a therapist that you can connect with and open up to. For me personally, therapy has not only changed my life, it has saved my life. Therapy can be such a huge factor in making progress when it comes to managing depression and anxiety. Our family paused financial contributions to our Roth IRA for about 6 months so that I could get the therapy I needed. And THAT’S OKAY!

Here’s how you can affordable, budget-friendly therapy!

I hope you find these five tips for managing your money and mental health helpful. Remember, our mental health comes before our financial health. However, we can do things TODAY to set our financial health up for success when our mental health waivers.

Today’s podcast episode is brought to you by my FREE debt free roadmap. Sometimes paying off debt is not as simple as it seems, especially if you are struggling with your mental health. It is incredibly helpful to have a guide to follow and a system for paying off debt you can set in motion when you are not in the throws of anxiety and depression. In this roadmap, I’m giving you the seven easy steps to follow that will set you up for success on your debt free journey. These are the steps that my husband and I followed to pay off over $111,000 worth of debt on 2 teacher salaries while growing our family. I’m also going to be sharing with you the three most common mistakes that hold people back from paying off debt so that you can avoid them! Plus, when you sign up for my debt free roadmap, you’ll get extra free resources sent straight to your inbox. Sound exciting? Sign up below!